Tracking Climate Action: How the World Can Still Limit Warming to 1.5°C Leave a comment

This article focuses on the 2023 findings of the annual State of Climate Action report series. View past articles here: 2022 | 2021 | 2020.

Today’s climate change headlines often seem at odds with each other. One day, it’s catastrophic wildfires wreaking havoc around the world; the next, it’s an optimistic piece on the rapid scale-up of solar and wind power. Taken together, such stories can make it challenging to understand the broader state of climate action. Are countries deploying climate solutions effectively if greenhouse gas (GHG) emissions are still rising? Where is the world making enough progress to overcome the climate crisis, and where are leaders falling short? What specific steps can get us on track?

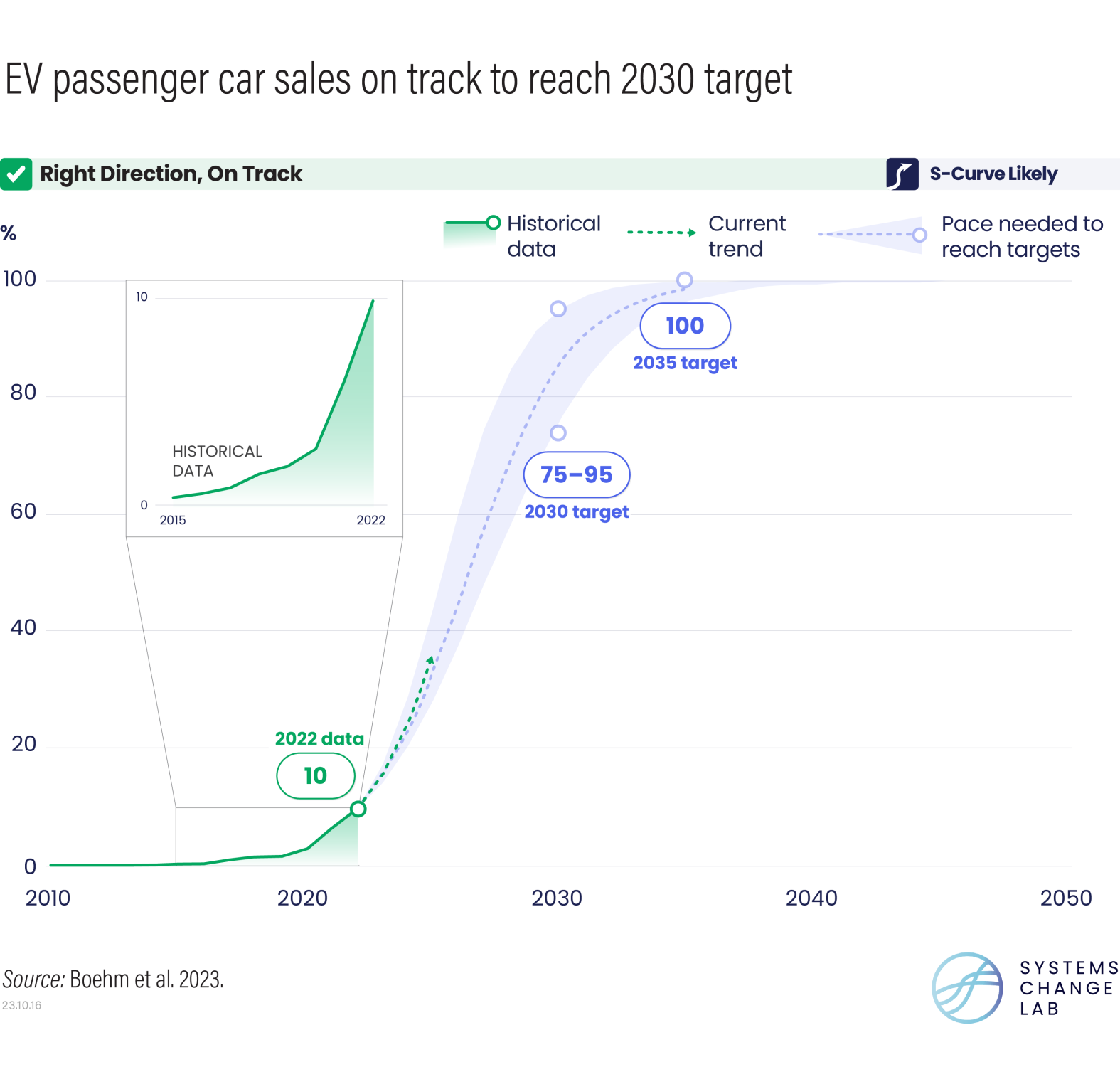

To help answer these questions, the State of Climate Action 2023 report provides a comprehensive roadmap of what’s needed by 2030 and 2050 to limit warming to 1.5 degrees C (2.7 degrees F), the limit scientists say is necessary for preventing increasingly devastating and irreversible impacts of climate change. It sets out the specific targets each sector will need to hit to achieve Paris Agreement goals and assesses where the world is today. This year’s analysis shows that of the 42 indicators of progress assessed, only one — sales of electric cars — is on track to reach its 2030 target and help keep 1.5 degrees C within reach.

In fact, progress for more than half of the indicators — including efforts to phase out coal in electricity generation, decarbonize buildings and reduce deforestation — remains well off track, such that the world will need to see at least a twofold acceleration this decade. For another six, recent trends are heading in the wrong direction entirely.

But it’s not all bad news: Over the past five years, the share of electric vehicles in passenger car sales grew exponentially at an average annual rate of 65% — up from 1.6% of sales in 2018 to 10% of sales in 2022 — putting this indicator on track for 2030. Global efforts are also heading in the right direction at a promising, albeit still insufficient, pace for another six indicators, including those focused on the scale-up of zero-carbon power, reforestation and mandatory corporate climate risk disclosure.

Of course, getting all indicators on track is ultimately what’s needed to protect people and nature from escalating wildfires, droughts, extreme storms and other climate impacts. This will require comprehensive action across every major sector — from food and electricity production, to transport, buildings, industry and ecosystem conservation.

Explore the interactive graphic below and read on for eight report findings showing where climate action currently stands across sectors — and what’s needed to get on track.

1) Global scale-up of zero-carbon power sources is advancing quickly, but fossil fuel phaseout in electricity generation is not.

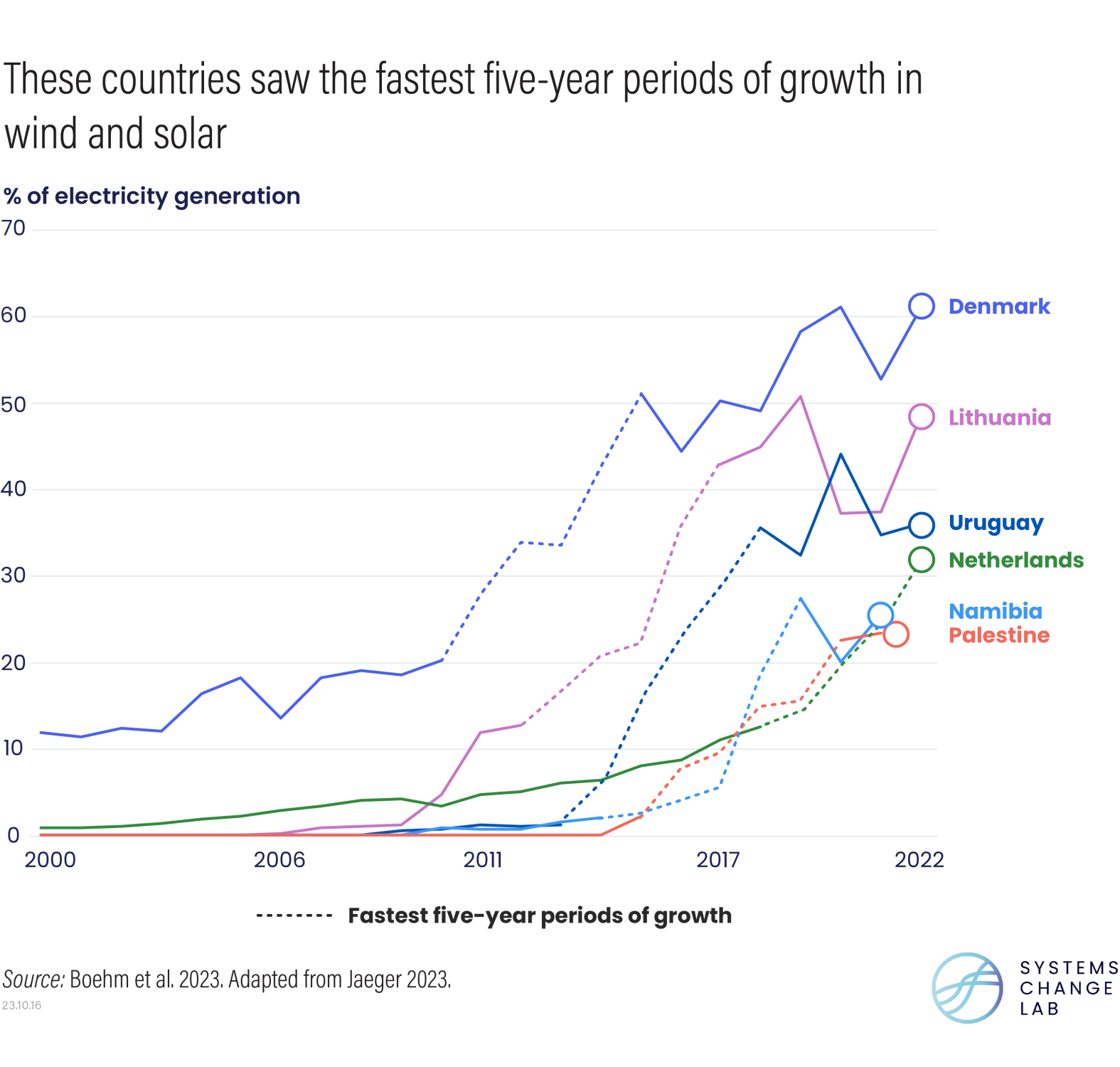

In 2022, carbon dioxide (CO2) emissions from electricity generation reached an all-time high, but rapid growth in both renewable energy installation and generation suggests that power sector emissions have plateaued and may start to fall this year. Zero-carbon technologies, such as solar and wind power, are widely mature and commercialized, and the cost of renewable energy, as well as complementary energy storage technologies, continues to plummet at unprecedented rates. Solar photovoltaics and onshore wind, specifically, are now the cheapest sources of new-build generation for at least two-thirds of the global population. Driven by these falling costs, recent years have witnessed record-breaking increases in adoption of these technologies, with strong evidence of ongoing exponential growth for solar.

Encouragingly, some of the fastest growth in renewable power generation has occurred across developing countries, such as Namibia and Uruguay, where wind and solar scale-up is also helping to bolster energy security and expand access to electricity. Achieving 1.5 degree C-aligned targets for zero-carbon power, however, will require such gains to accelerate dramatically — the global share of solar and wind in electricity generation has been growing by an annual average of 14%, but this needs to reach 24% by 2030.

Decarbonizing power will also require rapid declines in electricity generated from fossil fuels, but progress made in phasing out coal and gas lags far behind. While renewables are scaling up quickly, many countries are still investing in fossil fuel-powered plants. Today, just over 2,400 coal-fired power stations are in operation, with about another 530 new power stations in the pipeline. But to achieve compatibility with the Paris Agreement, the share of coal in electricity generation needs to decline seven times faster than recent rates — equivalent to retiring about 240 average-sized coal-fired power plants each year through 2030. At the same time, countries must also phase out unabated fossil gas more than 10 times faster to avoid locking in an emissions-intensive future.

2) Shifts to more sustainable modes of transportation, like bicycling, have yet to gain traction, but electric passenger car sales are taking off.

Rising incomes have increased travel and car ownership, driving steady growth in GHG emissions from transport. Global car ownership, for example, grew from about 240 vehicles per 1,000 people in 2015 to nearly 280 vehicles per 1,000 people in 2020, with especially high rates in developed countries.

Unsurprisingly, travel by private car continues to rise and remains stubbornly high in wealthy countries like the United States.

To reduce the number of kilometers traveled in these passenger cars, the world must shift to more sustainable modes of transportation — walking, bicycling and shared public transit. But in the highest-emitting cities, initiatives to expand bike lanes and public transit infrastructure, though heading in the right direction, remain far too slow. Together, these cities need to construct 140,000 kilometers of bike lanes and roughly 1,300 kilometers of metro rails, light-rail tracks and bus lanes each year through 2030.

While accelerating these modal shifts has proven challenging, the world has made considerable strides forward in electrifying existing forms of transport. Electric passenger car sales, for example, are on pace to reach their 1.5 degree C-aligned target for 2030. Declines in cost, improvements in range and the expansion of charging infrastructure have all contributed to this recent exponential growth, with Norway, Iceland, Sweden, the Netherlands and China witnessing the fastest increases. Gains made decarbonizing longer-haul transport like trucking, shipping and aviation, however, lag behind and will require more support to reach their 2030 targets.

3) After rising for decades, GHG emissions from buildings have stabilized, but such gains must accelerate significantly.

To spur further reductions in this sector’s GHG emissions, the world must implement a multipronged strategy to improve buildings’ energy efficiency, decarbonize the remaining energy used, retrofit existing buildings with zero-carbon technologies and ensure that new buildings are constructed to be zero-carbon in operation.

Additionally, emissions generated during construction must see rapid reductions, and the increasing use of fluorinated gases in cooling systems (which have considerably higher global warming potentials than CO2) needs to reverse course entirely. Publicly available data indicate that efforts made in delivering these much-needed changes by 2030, however, remain well off track.

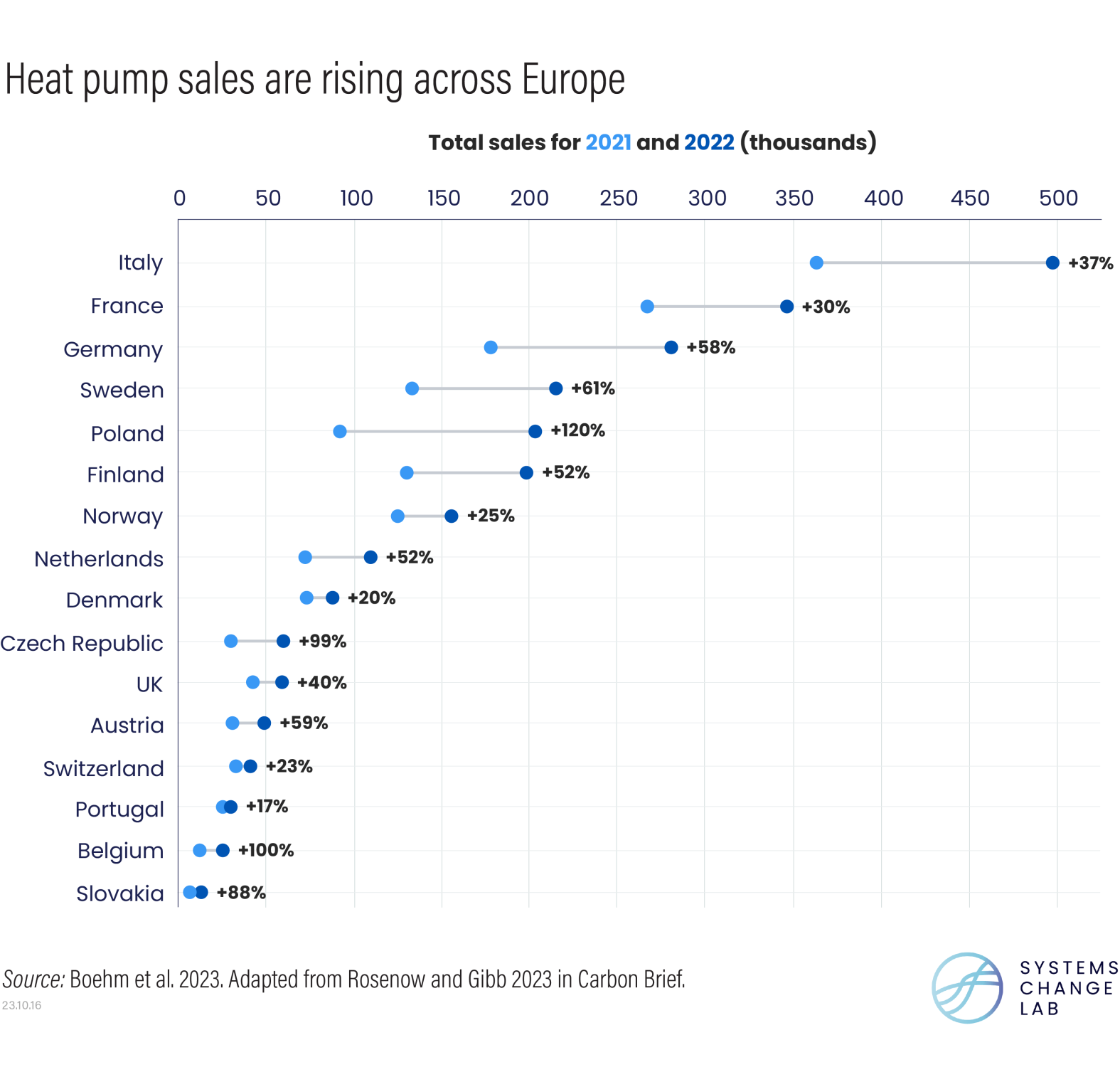

Still, a recent uptick in building regulations primarily within Europe suggests that some progress is underway. Grappling with an energy crisis following Russia’s invasion of Ukraine, the European Union, for example, proposed legislation that would ban the use of fossil fuels for heating in new and renovated buildings, as well as require a complete phaseout of fossil fuels for heating across all buildings by 2035. Similarly, sales of heat pumps — a technology that helps decarbonize heating systems — continue to increase, rising by 120% in Poland, 38% in Europe and 11% globally in 2022. Such advances now need to spread around the world.

4) Although progress decarbonizing steel and cement has largely stagnated, recent developments suggest the tide may soon turn.

Since 2000, GHG emissions from industry — which encompasses the production of materials like cement, steel and chemicals, as well as the construction of roads, bridges and other infrastructure — have increased faster than in any other sector.

Reversing this trend is possible, but there is no silver bullet. Instead, mitigating this sector’s emissions will require lowering consumption of products like cement and steel; improving energy efficiency across industrial processes and electrifying those that rely on low- and medium-temperature heat; and developing new solutions like green hydrogen for processes that cannot be easily electrified. Yet efforts to implement this decarbonization roadmap across cement and steel — two of the most emissions-intensive industries — remains well off track and heading in the wrong direction, respectively. Recent improvements in both indicators have stagnated, placing their targets for 2030 further out of reach.

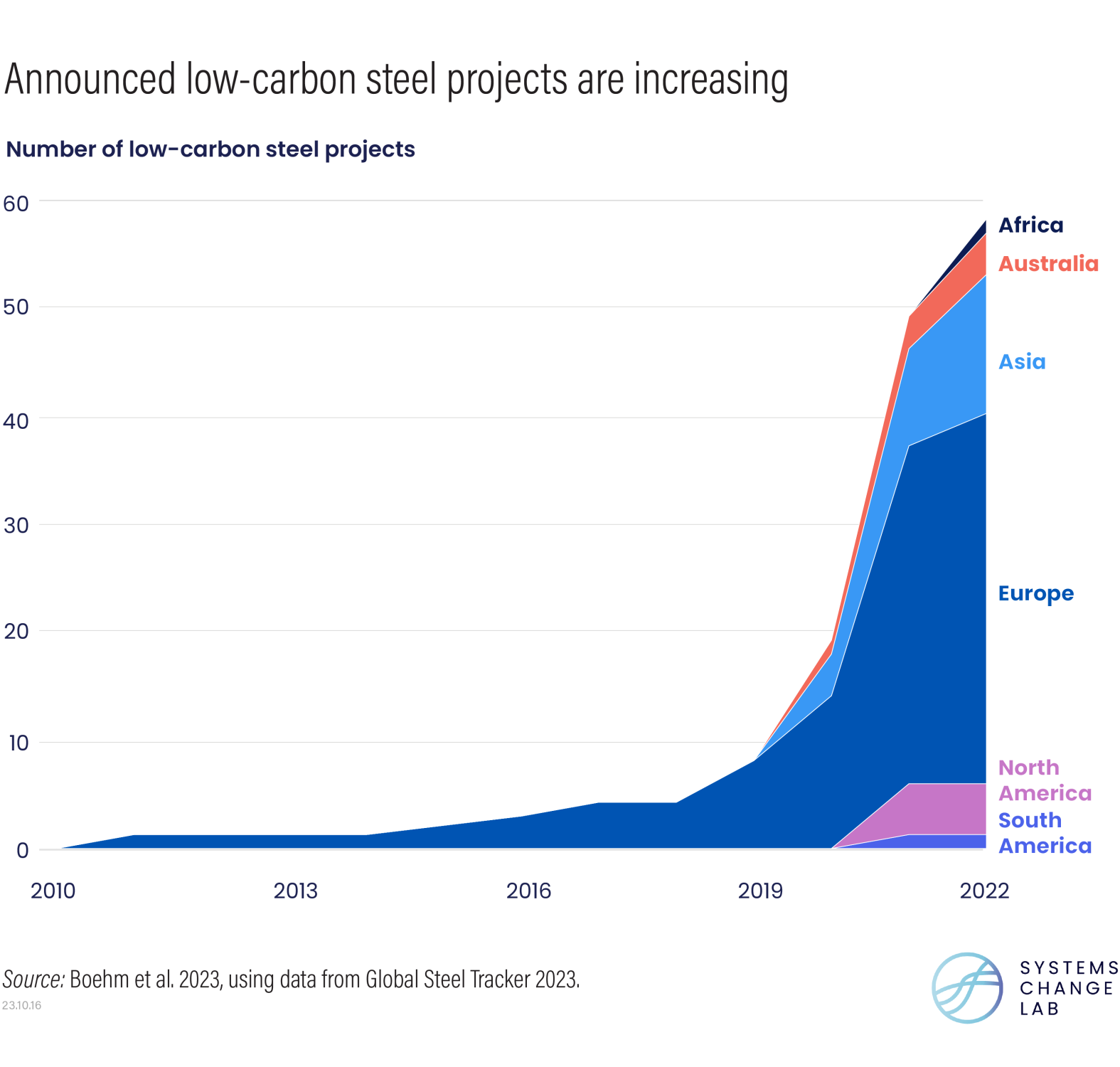

Some positive news, however, is emerging across these industries. The International Finance Corporation, the largest global development institution focused on the private sector in emerging markets, recently made its first green loan for material manufacturing in Africa to Senegal’s leading cement manufacturer. The government of India, home to one of the world’s fastest-growing industry sectors, announced that it will establish a carbon market scheme to help accelerate decarbonization of cement, steel and other industries. And globally, steel pipeline projects are shifting from production technologies that depend on coal to less emissions-intensive plants, with 28 new projects relying on green hydrogen announced between 2021 and 2022.

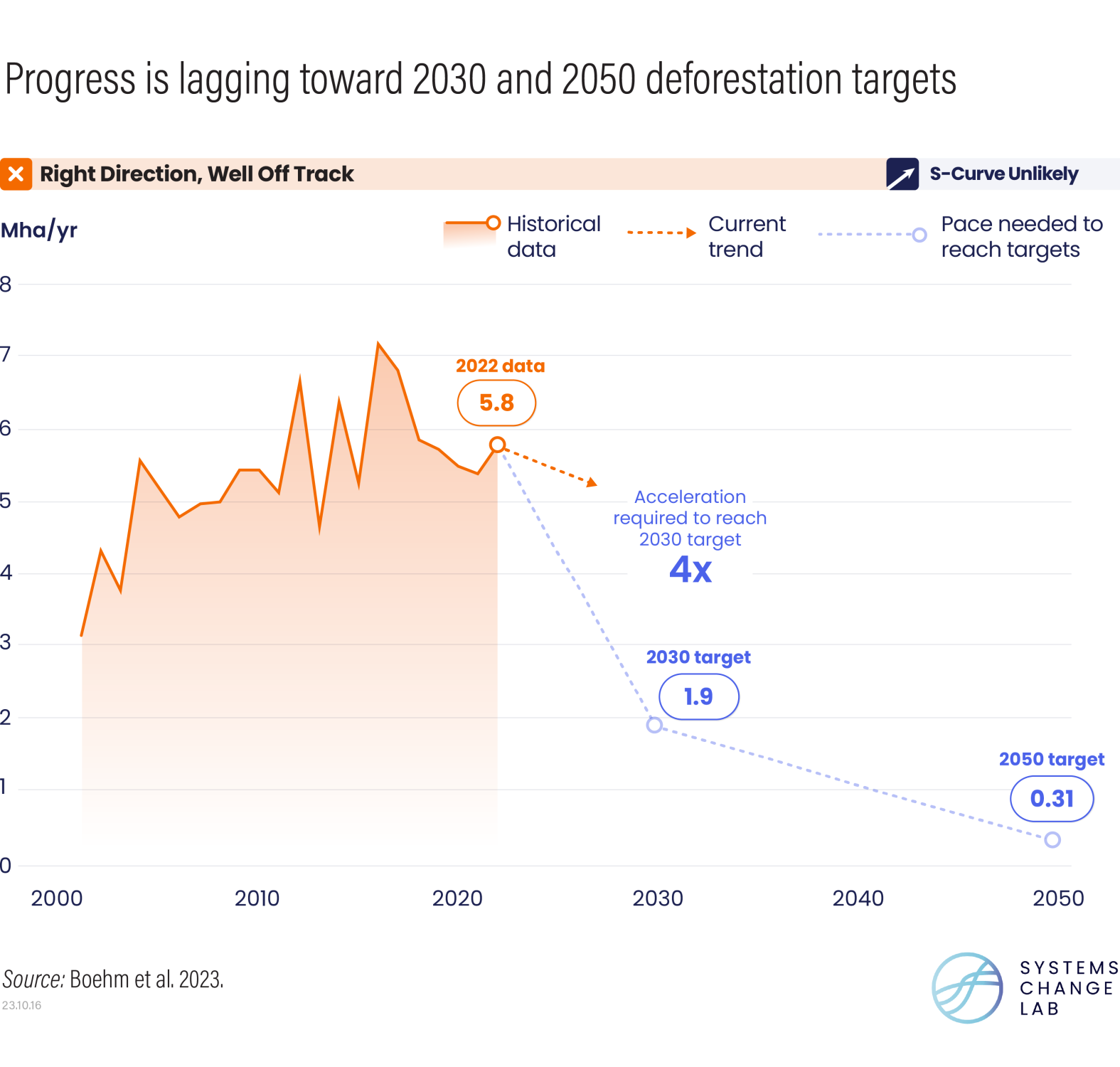

5) Conserving forests, peatlands and mangroves generates enormous climate benefits at relatively low costs — yet efforts to protect and restore these ecosystems remain dangerously off course.

Together, the world’s forests, peatlands and mangroves hold well over 1,000 gigatons of carbon, and roughly a third or less of these carbon stocks (340 gigatons of carbon) are vulnerable to disturbances, such that they would be released into the atmosphere following conversion or degradation. Some of these carbon losses can occur quite rapidly, and if released, much of this carbon would be difficult for ecosystems to recover on timescales relevant to reaching net-zero CO2 emissions by midcentury. Fully rebuilding these carbon stocks would take 6 to 10 decades for forests, well over a century for mangroves, and centuries to millennia for peatlands.

It is alarming, then, that the world lost roughly 15 football (soccer) fields of forests per minute in 2022, that 57 million hectares of peatlands (an area roughly the size of Kenya) are currently degrading and that shorelines have lost 560,000 hectares of mangroves since 1999.

A wave of recent developments offers some good news, particularly for the world’s forests. Since COP26, over 140 countries pledged to halt and reverse forest loss and degradation under the Glasgow Leaders’ Declaration on Forests and Land Use. Nearly 190 parties committed to protecting 30% of the planet and restoring another 30% of degraded ecosystems by 2030. Within days of his inauguration, President Luiz Inácio Lula da Silva undertook a range of actions to combat deforestation across the Brazilian Amazon. In light of Indonesia’s historically low levels of deforestation, the government signed another forest finance deal with Norway. And the European Union recently adopted a regulation to combat deforestation and forest degradation associated with commodities.

While these changes are promising, history must not repeat itself. Interim targets under the New York Declaration on Forests and the Bonn Challenge, for example, were missed, while pledged funds to protect and restore ecosystems have yet to fully materialize.

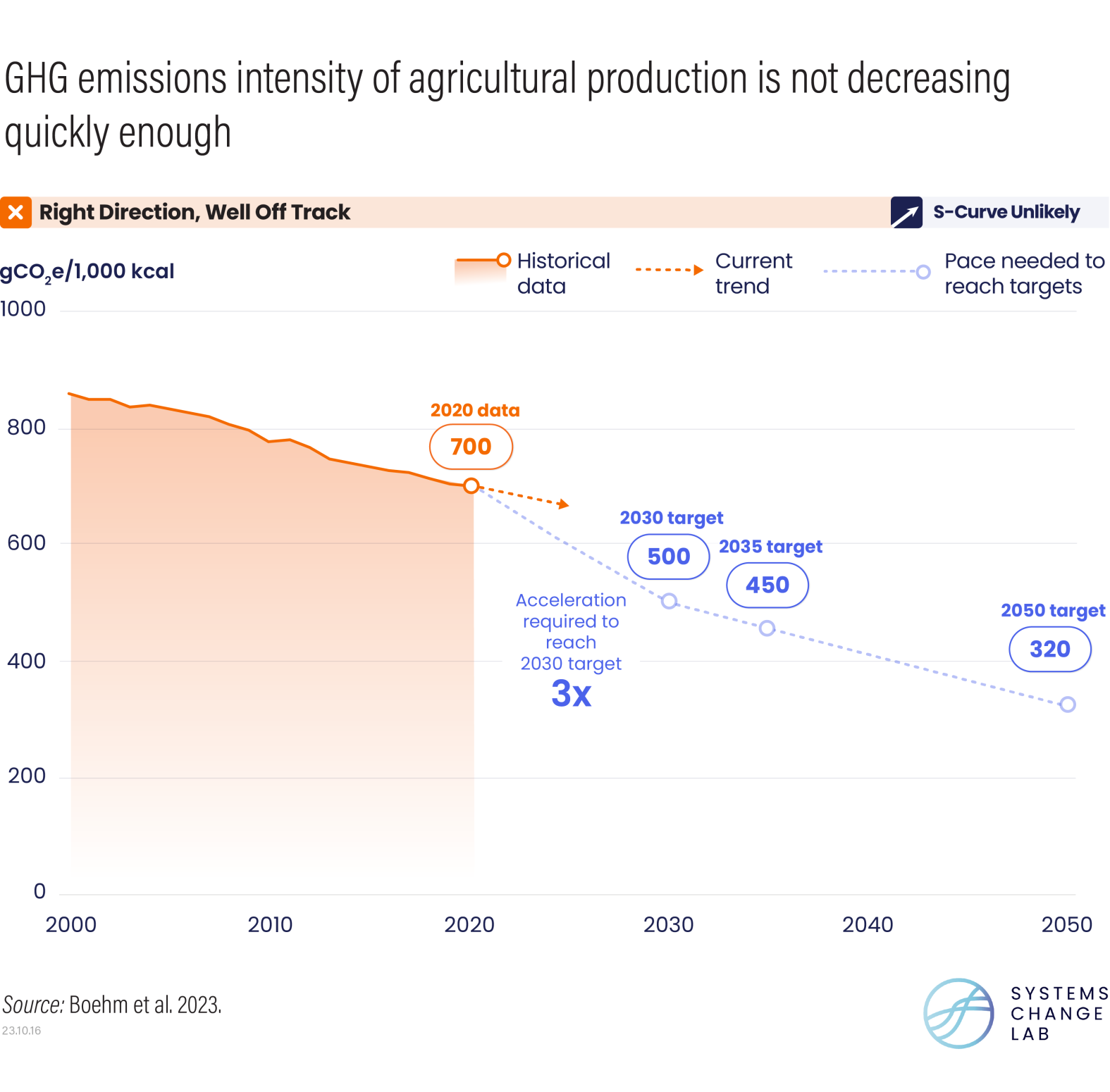

6) Lackluster progress risks placing most food and agriculture targets out of reach.

Within the next three decades, the world must feed nearly 10 billion people more nutritiously, while also eliminating poverty, virtually halting deforestation and degradation, and lowering GHG emissions from agricultural production. Achieving these goals will require immediate action across supply chains. In the face of climate impacts that threaten to dampen yields, farmers must produce more food on fewer hectares to avoid clearing forests for new fields and pastures. At the same time, they must also reduce GHG emissions from a range of agricultural practices, such as those associated with rice cultivation, livestock production and fertilizers.

Though heading in the right direction, recent trends in these supply-side shifts remain too slow. Improvements in livestock production efficiency and crop yields, for example, have failed to keep pace with growing demand for food, and continued farmland expansion undermines efforts to protect and restore ecosystems. Global increases in crop yields need to accelerate more than 10 times faster and gains in livestock productivity must occur 1.2 times faster to help limit warming to 1.5 degrees C. Efforts to reduce the amount of GHGs emitted per calorie of food produced also remain far below the required pace, such that recent rates of change must accelerate threefold over this decade.

Demand-side shifts can also help mitigate this sector’s emissions. Halving food loss and waste by 2030, as well as reducing beef, lamb and goat consumption to roughly two servings per week or less by 2030 and 1.5 servings per week or less by 2050 across high-consuming regions (the Americas, Europe and Oceania), can help lower the emissions intensity of food systems. While the data is insufficient to assess global changes in food waste, trends in the share of food loss are now heading in the wrong direction, and shifts to more sustainable diets, though moving in the right direction, must occur eight times faster to get on track.

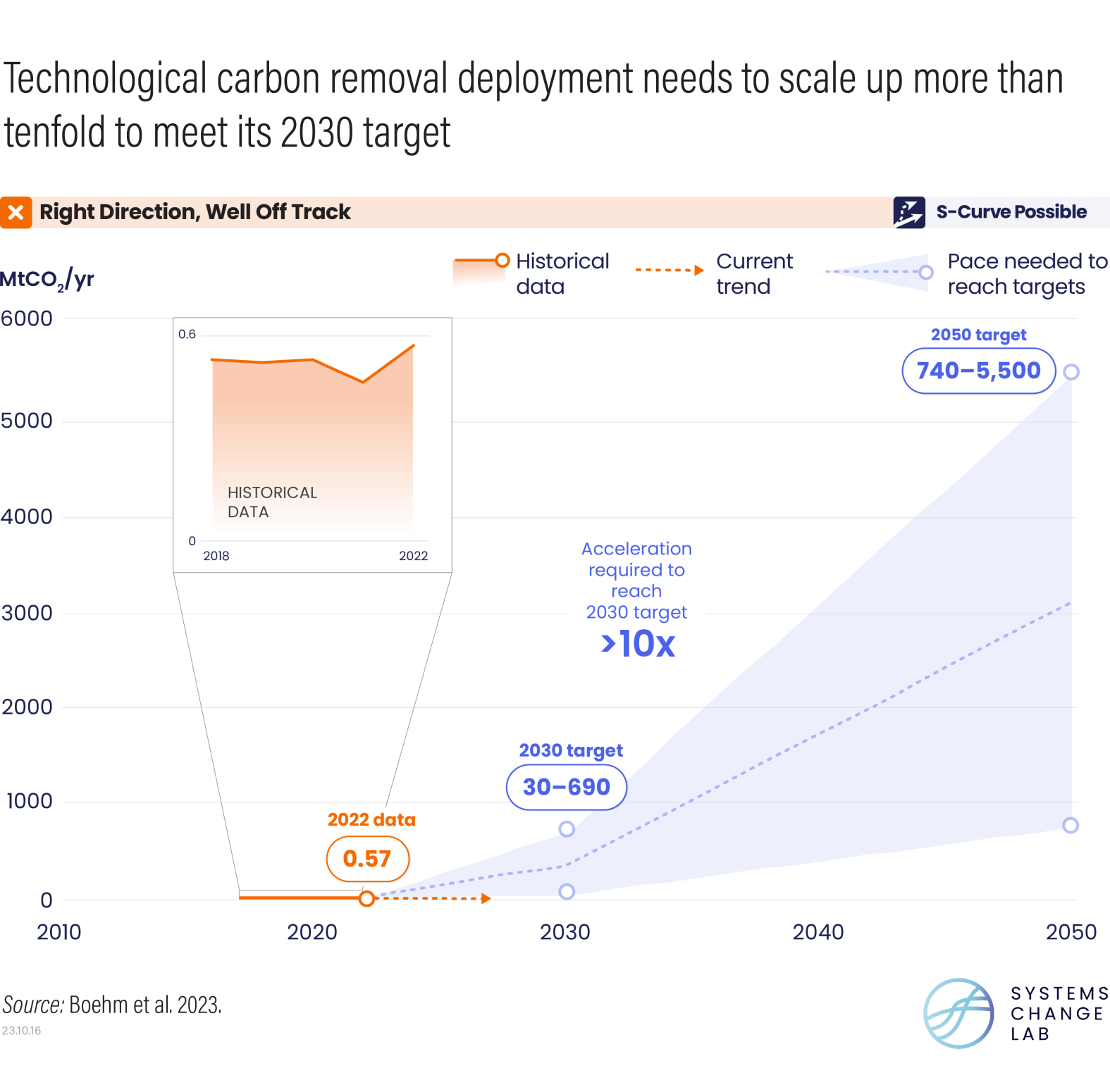

7) Technological carbon removal approaches today sequester less than 1% of the amount needed in 2030, but momentum behind them is growing rapidly.

The Intergovernmental Panel on Climate Change finds that, alongside immediate and steep reductions in GHG emissions, limiting warming to 1.5 degrees C with no or limited overshoot now relies on carbon removal, including both land-based measures like reforestation and technological approaches like direct air capture (DAC). By 2030, technological carbon removal rates, specifically, need to reach between 30 and 690 metric tons of carbon dioxide (MtCO2) per year, but in 2022, less than 1 MtCO2 was removed. To get on track for 2030, these technological approaches must scale up more than 10 times faster.

Fortunately, technological carbon removal approaches have evolved from a niche concept to a common component of climate action portfolios in recent years, supported by billions of dollars in public and private funding. In the United States, the 2021 Bipartisan Infrastructure Law provided $3.5 billion to build four DAC hubs that can each remove 1 MtCO2 annually, and the 2022 Inflation Reduction Act more than tripled the tax credits that DAC operators receive. In 2022, an international coalition of companies committed to buy more than $1 billion worth of permanent carbon removal by 2030. To continue building this momentum, more public funding for research, development, demonstration and deployment is needed to create a diverse portfolio of approaches that balances the tradeoffs of each. To ensure a responsible scale-up, governments must also develop robust governance frameworks, for example, by establishing consistent and credible standards to measure carbon removal and by focusing attention to environmental and social impacts of projects.

8) Climate finance, especially in developing countries, pales in comparison to estimated needs, while public financing for fossil fuels is increasing.

Finance is a vital enabler of climate action, but current investment patterns are hindering the pace and scale of the transition to net-zero economies. Global tracked climate finance, including both domestic and international flows from public and private sources, reached an all-time high of $1.4 trillion in 2022, according to new data that Climate Policy Initiative published after the 2023 State of Climate Action report went through peer review. Yet such gains remain far short of the $5.2 trillion per year needed by 2030. Instead flows must increase by nearly half a trillion each year through this decade to get on track.

Finance needs are particularly acute in developing countries, where intensifying climate impacts, the COVID-19 pandemic, unsustainable debt burdens and food and energy price spikes following Russia’s invasion of Ukraine are stretching government coffers. When excluding China, investments in developing countries are less than a tenth of the $2.4 trillion per year that they need to mitigate and adapt to climate change by 2030.

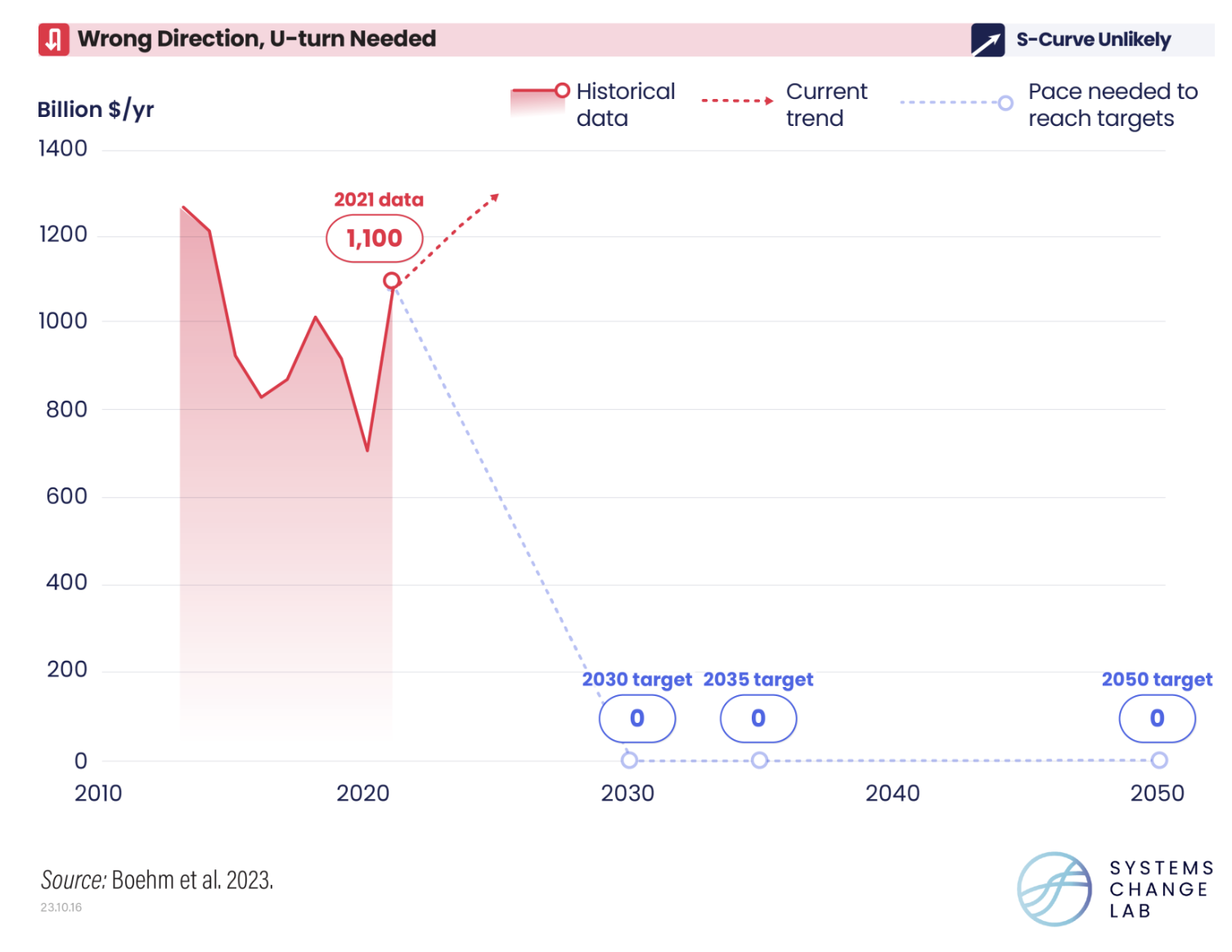

Increasing climate finance without simultaneously phasing out investments in high-emissions activities, such as fossil fuel extraction and deforestation, will not reduce GHG emissions rapidly enough to limit warming to 1.5 degrees C. Here too, progress remains inadequate. Though worldwide investments in low-carbon energy supply exceeded those in fossil fuels for the first time in 2022, recent progress must accelerate more than tenfold by 2030.

Worse still, public financing for fossil fuels rose to $1.1 trillion in 2021 — a concerning reversal in recent trends. Meanwhile, efforts to expand carbon pricing appear stalled, with no significant increase in global GHG emissions covered by pricing systems since 2021. Such delays in aligning finance with the Paris Agreement will impede climate action across all sectors.

COP28 and the Road Ahead for Climate Action

As the first Global Stocktake under the Paris Agreement draws to a close at this year’s UN climate summit (COP28), world leaders must recognize the largely sluggish pace of climate action to date and chart a path forward that builds on today’s bright spots. This moment must serve as a springboard for accelerated actions to mitigate climate change — including equitably phasing out fossil fuels and scaling renewable energy, transforming the food and agriculture sector while halting and reversing deforestation, and scaling and shifting finance — in addition to those focused on enhancing adaptation and responding to losses and damages.

We know that with the right support, transformational change can take off, and we have a clear roadmap to follow to limit warming to 1.5 degrees C. It’s not too late.

This article is part of the Systems Change Lab, a collaborative initiative — which includes an open-sourced data platform — that is designed to spur action at the pace and scale needed to limit global warming to 1.5 degrees C, halt biodiversity loss and build a just and equitable economy.

View past State of Climate Action Insights articles here: 2022 | 2021 | 2020.

Courtesy of WRI.

By Sophie Boehm, Clea Schumer, Emma Grier, Louise Jeffery, Judit Hecke, Joel Jaeger, Claire Fyson, Kelly Levin, Anna Nilsson, Stephen Naimoli, Emily Daly, Joe Thwaites, Katie Lebling, Richard Waite, Jason Collis, Michelle Sims, Neelam Singh, William Lamb, Sebastian Castellanos, Anderson Lee, Marie-Charlotte Geffray, Raychel Santo, Mulubrhan Balehegn, Michael Petroni, and Maeve Masterson

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

EV Obsession Daily!

I don’t like paywalls. You don’t like paywalls. Who likes paywalls? Here at CleanTechnica, we implemented a limited paywall for a while, but it always felt wrong — and it was always tough to decide what we should put behind there. In theory, your most exclusive and best content goes behind a paywall. But then fewer people read it!! So, we’ve decided to completely nix paywalls here at CleanTechnica. But…

Thank you!

Iontra: “Thinking Outside the Battery”

Advertisement

CleanTechnica uses affiliate links. See our policy here.